Out of breath. That’s probably the first association that comes to my mind when I hear the word ‘bank’. And who can judge me? After all, that’s exactly what my seven-year-old eyes saw when waiting for my parents to cash out their paychecks. People limited by the banks’ inconvenient schedule, trying to catch their breath as they waited for hours (seated if lucky) to get hold of their salaries or pensions, send money to relatives, or simply get a statement. By that time, my interests weren’t much besides playing video games and watching cartoons. I knew nothing about banking, marketing, or customer satisfaction. Yet, it didn’t take a degree to sense something was off about the whole experience. Today, I can assert that instinct was right.

The Fintech lessons: don’t overlook technological breakthroughs

It was that bad experience that initially drew me (along with thousands of other professionals) to the fintech industry. The idea of improving banking by leveraging technologies and implementing a client-centric approach to all services seemed fascinating. And it was — so much that fintech has become one of the hottest high-growth sectors in the past decade.

In 2021 alone, global fintech funding amassed a record-breaking $132 billion. And if that figure doesn’t speak to you, maybe the fact that $1 out of $5 VC dollars worldwide goes to fintech will be eyebrow-raising enough. But what’s more surprising (or not) is that it hasn’t been the established banking institutions that led the race for innovation. No, the game changers felt a lot more than IT companies taking the lead rather than financial institutions. Digital banks and neobanks embraced the ‘fewer branches, better apps’ motto and taught a lesson to the big banks on how to serve the younger clients. According to a recent study, Gen Z is considerably less likely to hold a traditional bank account compared to Millennials or Baby Boomers.

Just 47% of Gen Z respondents — versus 75% of Baby Boomers and 70% of Millennials — claimed to have an account with a traditional bank, or credit union.

It was a good lesson for banks. In the past decade, fintech has turned the banking industry upside down, pushing even the most traditional institutions to create smoother banking experiences through browser and mobile applications. Banks learned that looking the other side comes at a cost far too great. Now, being a lot more reactive to technological breakthroughs and customer needs, banking executives are eyeing (you guessed it right) the metaverse. But… is it really worth it? Short answer: yes.

As someone that works for a metaverse developing company, it would be strange to say otherwise. Fair enough. Yet, that doesn’t change the fact that the metaverse remains a widely underdeveloped concept. And that’s okay. The Internet was an underdeveloped concept only a few decades ago. And here we are now — having panic attacks when we cannot find a decent Wi-Fi. Yet, our Internet addiction isn’t a valid argument. The numbers, well, that’s another story.

“The Metaverse market may reach $783.3 billion in 2024 vs. $478.7 billion in 2020 representing a compound annual growth rate of 13.1%,” reports Bloomberg.

According to Bloomberg Intelligence, data from Newzoo, IDC, PwC, Statista and Two Circles are pointing to a massive expansion in the years ahead. From a nearly $800 billion market size estimated by 2024, half of the metaverse size value is linked to the potential growth for gaming, AR, and VR applications in this new realm.

Right, bankers are not joining the metaverse to play Beat Saber. While there’s a “self-improvement” angle to the decision, growth is always at the core. Time to examine potential reasons for bankers to join the alternate virtual universe.

1. Strategic positioning for MetaFi

We are not headed to the metaverse. Many of us are already interacting with metaverses on a daily basis. If you ever played Minecraft or any other MMORPG (Massively Multiplayer Online Role Playing Games), chances are the concept of a metaverse isn’t new to you at all.

The difference between what crypto bros advocate and the metaverses we already know is the paradigm they belong to. The bulk of games and social experiences we use today are part of Web 2.0 — a standard dominated by centralized platforms and a regulated fiat financial system. The new generation of metaverses, like Sensorium Galaxy, Decentraland, and Sandbox, are part of Web 3.0, a model built around user privacy, data ownership and decentralization. And whenever we talk about decentralization, we talk about blockchain.

Blockchain is a core pillar of Web 3.0 as it offers a transparent and reliable decentralized infrastructure. When it comes to handling the economies of these new virtual environments, it’s a perfect match. Instead of using in-game currencies and assets controlled by game developers, participants can manage their funds through blockchain-based currencies and NFTs, moving in-and-out of these economies seamlessly and accessing a wide array of compatible financial services.

MetaFi (Metaverse Finance) stands as a logical step in the development of DeFi (Decentralized Finance). With the value of fungible and non-fungible assets secured by blockchain, DeFi protocols and services can easily power metaverse economies. For instance, using your NFTs as collateral for a cash loan. Or earning interest by staking in-game currency.

But… How do banks fit into this picture? As of today, they kind of don’t fit at all. Blockchain isn’t yet part of their everyday vocabulary for many banks, especially retail ones. That might, however, change in the near future as central banks are speeding up their efforts to develop so-called Central Bank Digital Currencies.

These government-backed, regulated digital currencies could be a catalyst for banks to enter the metaverse party in full swing, and therefore giving them enough flexibility to run experiments that directly involve DeFi solutions.

As outlined in the paper “Lessons Learned from Decentralised Finance” by ING: “It is uncertain if DeFi protocols are actually in direct competition with banks at all [...] protocols for loanable funds are not directly acting as a full-fledged replacement for banks, because traditional banks are not intermediaries of loanable funds: rather, they provide financing through money creation”.

2. Building up brand awareness

With the metaverse being at such an early stage of development, putting your name out there isn’t very difficult nor expensive, especially if you’re a deep-pocketed bank. Proof? How about this headline: “With a tiger and Jamie Dimon, JPMorgan enters the metaverse”. For fair reasons, some of you may associate such a story with a plain PR stunt leveraging the latest digital trend rather than a comprehensive awareness campaign. Yet, it’s worth looking twice.

Despite Dimon’s lack of enthusiasm when it comes to the crypto world, he seems to understand the value of digital currencies as a value transfer mechanism.

“If you said to me, ‘I want to send $200 to a friend in a foreign country,’ that could take you two weeks and cost you $40. You could do it through a digital currency, and it’ll take you seconds,” said Dimon in a recent interview.

With JPMorgan’s Onyx virtual lounge on Decentraland, the bank capitalizes on its crypto-friendly audience and introduces participants to Onyx — the bank’s innovative blockchain-based platform for wholesale payments transactions.

True. The users of Decentraland are most certainly not the target audience of Onyx services. But that was never the point. For JPMorgan, the real gain is perception. Now, whenever we think of banks, crypto and metaverses, the Onyx case is top of mind. Need a bank that understands the specifics of metaverses and the Web3 reality? “Look no further…”

3. Humanizing customer experience

Strategic positioning and brand awareness are without a doubt valid reasons for bankers to experiment with metaverses. But there’s a more pragmatic motive: customer experience.

Let me ask you this: do you perceive Gen Z as the type of clients that would visit bank branches? Yes, we are talking of a generation that trusts traditional banks less, relies mostly on digital services, and demands further developments in the virtual space.

One could be easily drawn to the conclusion that Gen Z falls under the category of ‘branchophobes’. I know I was. However, that isn’t really the case.

A research by Cornerstone Advisors outlines that the young public remains bullish on branches. Why? The poll results point to two main reasons:

- Digital experiences offered by banks are falling short of expectations

- Young clients still want to get their affairs sorted out by humans.

Can we judge them? Probably not. If there’s one thing more irritating than Youtube advertisements, it’s customer service chatbots. And when it comes to dealing with people’s money questions, conversational AI seems to be falling really short.

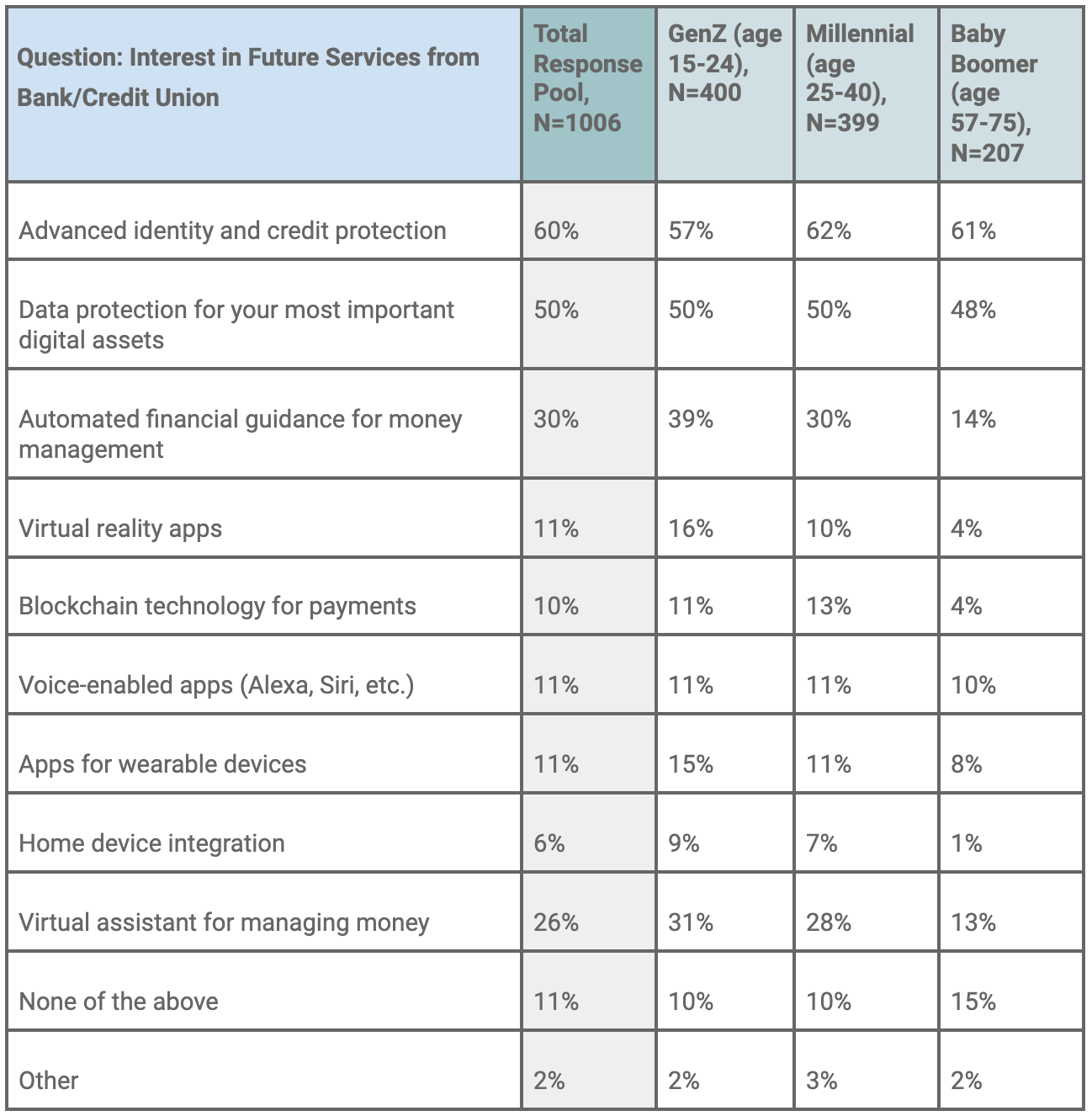

A survey by live-chat provider GoMoxie found that 60% of banking customers aren’t satisfied with customer service chatbots and don’t trust them. In a similar study by research firm Phoenix Synergistics, only 26% of consumers using AI-powered chatbots reported to be very satisfied. Unsurprisingly, Gen Z desires for future bank services the highest interest in virtual reality applications, alongside with virtual assistants and automated guidance for money management. The digital native generation believes that VR can help businesses ‘humanize’ customer service. And in times of COVID-19 and Monkeypox, that wouldn’t hurt.

Some institutions are already experimenting in this area. South Korea’s Kookmin Bank is allowing one-on-one meetings between customer and employee avatars in its virtual bank.

Bottom line: bankers are trying, and so should everyone

If we think of the Metaverse as the next generation of the Internet, then banking (and every other sector really) is up for a change. From services accessibility to customer experience to decentralized services, the metaverse and the new Web 3.0 paradigm will reshape our relationship with money and, therefore, the services built around it.

Unlike with the mobile revolution, banks aren’t ignoring this technological breakthrough. That’s the Fintech lesson we’re all thankful for. With the metaverse still in its early days, there are great opportunities that arise from the transformation of our digital lives. And staying out of that process is, if anything, a misguided decision.

Banking is very good business if you don’t do anything dumb. — Warren Buffet.

An Op-Ed by Matias Lapuschin, Head of Content at Sensorium

Disclaimer: This is an op-ed. Neither the opinions expressed by the author, nor the conclusions drawn in this article, reflect the opinions, viewpoints, or beliefs of Sensorium, its staff, or any organizations with which Sensorium is affiliated.

{kind=link}